Every industry is feeling the impact of an ever-changing trade environment, but the retail supply chain has been hit by two forces simultaneously: the broad impact of tariffs affecting all sectors and the end of the de minimis exemption that uniquely devastated cross-border e-commerce volumes.

Purolator commissioned HelloInfo to independently survey 348 shipping and logistics decision-makers across industrial, retail, healthcare and technology in Canada and the United States. Across 41 in-depth interviews and quantitative data from 90 retail respondents, one finding defined the retail picture more than any other: The end of the de minimis exemption has changed the rules of cross-border e-commerce. The retail companies handling it best are the ones that recognized early that these changes are a foundational shift in cross-border retail trade as we’ve known it.

This article dives into what the data shows about the current state of retail trade, how North American retailers are responding to tariffs and changing trade rules, and what every retail shipper needs to know before the upcoming CUSMA/USMCA review.

“I do have an official do-not-buy American mandate. We are developing a turnkey distribution strategy for Western Canada and one of the best contenders is a huge company over 15,000 employees, but they are based in the United States.” — Canadian retail company

Key takeaways

-

- The impact of tariffs on retail supply chains in Canada and the United States

- Tariff mitigation strategies North American retailers have taken in the past 18 months

- Why retail is the least-prepared sector for the CUSMA/USMCA review

- How retail companies plan to insulate themselves from future tariff impacts

- What retail shippers need from their logistics partners

- How Purolator can help retail companies get ready for July’s CUSMA/USMCA review

The impact of tariffs on retail supply chains in Canada and the United States

Retail has entered the current trade environment carrying a burden that no other sector feels in the same way. General tariff pressure—the cost increases, supply chain disruptions and planning uncertainty that industrial, healthcare and technology companies are also absorbing—has hit retail hard. But retail is the only sector simultaneously facing the end of the de minimis exemption, a change that restructured the economics of cross-border e-commerce in ways that tariff rates alone haven’t replicated elsewhere.

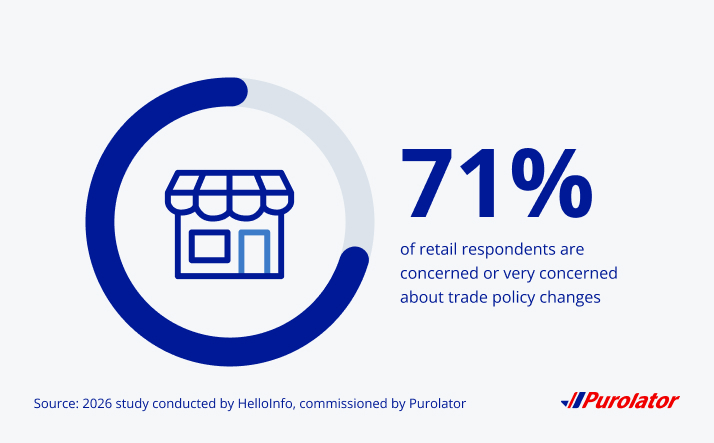

Seventy-one percent of retail respondents describe themselves as “concerned” or “very concerned” about trade policy changes. Tariff costs are ranked as the top concern by 44% of retail respondents, followed by overall shipping cost increases at 14%. And 76% say trade policy changes have had a moderate or significant impact on business planning, with 28% reporting a significant impact.

Learn how to minimize the impact of tariff changes

What the de minimis exemption was and what its elimination means for retail

The de minimis exemption, established under Section 321 of the U.S. Tariff Act, previously allowed shipments valued under $800 USD to enter the United States duty-free with minimal customs documentation. For cross-border e-commerce retailers shipping individual orders from Canadian or international warehouses directly to U.S. customers, this exemption made their business model work.

As of August 2025, that exemption is gone. All commercial shipments into the U.S., regardless of value, are now subject to duties and full customs clearance procedures. Shipping volumes are shifting for most retailers, with over 60% of respondents across industries reporting inbound or outbound volume changes due to tariffs—particularly among Canadian firms. One retail respondent confirmed shutting down U.S. shipping entirely. Another is taking on hundreds of millions of dollars in new costs. Canadian companies are weighing fulfillment and warehouse investments in the U.S. to reduce border crossing frequency, but they’re hesitant to invest in decisions of that scale while trade policy remains unsettled.

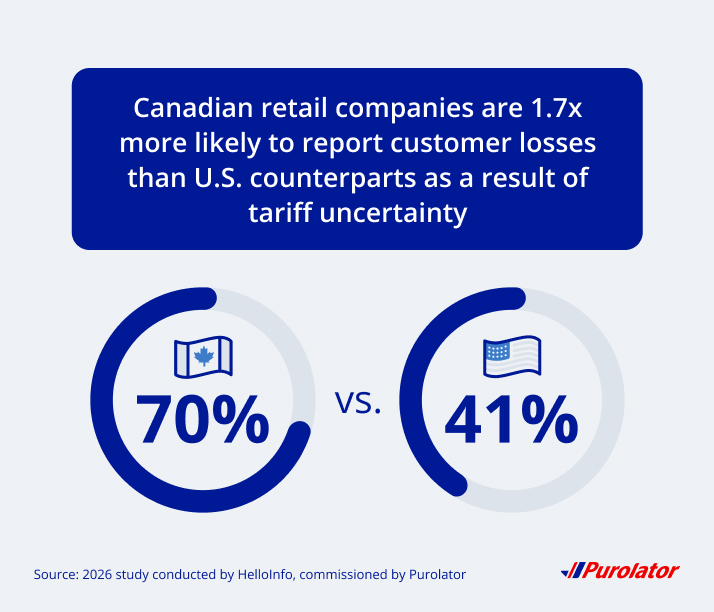

Customer loss is highest in Canadian retail

Companies across industries have lost customers as a result of tariff uncertainty, but the gap between Canadian and U.S. retail companies is one of the widest of any sector in the research. Canadian retail companies are 1.7 times more likely to report customer losses than their U.S. counterparts (70% vs. 41%). That gap reflects both the volume disruption caused by the end of de minimis exemptions and the two-front tariff pressure that Canadian retailers face. They’ve been hit by U.S. tariffs on exports and retaliatory Canadian tariffs on U.S. imports at the same time.

CUSMA/USMCA certification offers limited protection for retail

Unlike industrial and healthcare companies, which have leaned heavily on CUSMA/USMCA certification as a cost mitigation tool, retail has limited access to tariff protections. Most retail sourcing originates in Asia where CUSMA/USMCA coverage doesn’t apply, so retail companies can’t easily use certification as a buffer against tariff exposure the way other sectors can. Retail is entering the CUSMA/USMCA 2026 review with fewer options for adaptation if the outcome isn’t in their favour.

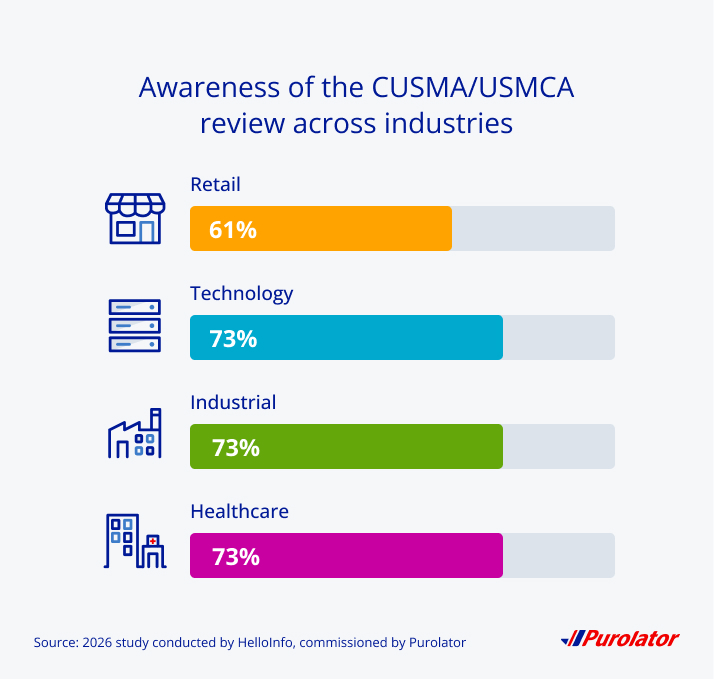

On top of this, retail has the lowest awareness of the upcoming CUSMA/USMCA review of any sector: 61% compared to 73% for technology and 74% for both industrial and healthcare. For a sector that’s highly exposed to a negative review outcome, that awareness gap translates directly into a lack of preparedness.

Read the full global trade report

Tariff mitigation strategies North American retailers have taken in the past 18 months

Despite their lower awareness of the CUSMA/USMCA review, retail companies in both countries have made significant operational changes over the past 18 months. They’re adjusting pricing strategies through price increases, margin pressure and ongoing supply chain reviews, and rethinking their retail supply chains. That said, Canadian and U.S. retail companies are prioritizing different actions based on the distinct pressures they’re each facing.

Discover options for mitigating tariff fallout

Where U.S. retail leads in response to tariffs

U.S. retail companies are reducing direct tariff exposure through sourcing pivots and infrastructure changes. They’re more likely to have switched suppliers (55% vs. 48% for Canada) and relocated distribution centres (34% vs. 24%), moves that have a more immediate impact on duty outlays.

Learn more about the U.S. response to tariff uncertainty

Where Canadian retail leads in response to tariffs

Canadian retail companies are taking more structural action. Seventy percent of Canadian retail respondents have adjusted shipping to and from the U.S. as a result of tariffs changes and the end of de minimis. Among those, the biggest moves already made include decreasing the use of U.S.-based suppliers (59%) and moving warehouse or processing facilities to Canada (56%).

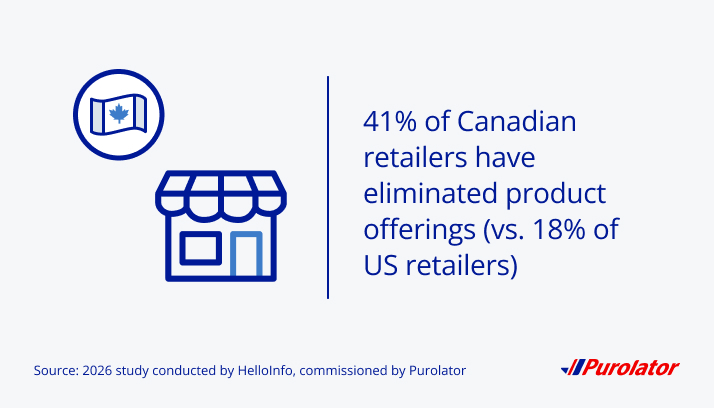

Retailers in Canada are also more than twice as likely as U.S. peers to have eliminated product offerings (41% vs. 18%), more likely to have invested in strategic customs practices (46% vs. 41%) and more likely to have relocated manufacturing (28% vs. 20%) or exited markets (30% vs. 20%). The product elimination gap in particular shows that Canadian retailers are simplifying what they sell and where they sell it, likely because the compounding pressure of costs rising from both directions has made complex retail supply chains unaffordable.

Learn more about the Canadian response to tariff uncertainty

Where Canadian and American retail companies align on tariff action

Routing changes are nearly identical across both countries (55% Canada vs. 57% U.S.), a consistent finding across all industries in this research that suggests this is a universal response to tariff pressure rather than a country-specific strategy. Market exits are concentrated in China and other APAC sourcing markets, with Canadian retail companies also pulling back from U.S. market exposure entirely in some cases.

Smaller businesses across industries are beginning to explore CUSMA/USMCA certification now that escalating tariff costs have made the administrative overhead worthwhile, with 67% of retail respondents actively leveraging certification. Many also rely on broker and shipping partners to stay current on trade developments rather than building internal compliance infrastructure. This differs from larger industrial and technology companies that have invested more heavily in in-house trade expertise.

Explore options for reshoring and nearshoring

Why retail is the least-prepared sector for the CUSMA/USMCA review

The CUSMA/USMCA review is scheduled for July 1, 2026. For retail, the sector with the most to lose from a negative outcome and the least visibility into what that outcome might be, now’s the time to get ready.

Even though two-thirds of retail companies are actively leveraging CUSMA/USMCA certification, awareness of the review itself sits at just 61%, which is the lowest of any sector. It’s an interesting paradox: They’re using the agreement while paying limited attention to its future—and this is retail’s largest vulnerability heading into the review. It’s not that retail companies are indifferent, but most are operating without the internal infrastructure to monitor what’s coming. Instead, they’re relying on external partners to keep them updated.

Despite low awareness, retail companies are reasonably optimistic about the review’s outcome. In Canada, technology and retail respondents are the most optimistic sectors about the renegotiation, in contrast to industrial and healthcare peers. But optimism built on limited information is not the same as confidence built on preparation. Companies that haven’t modelled what a negative outcome would mean for their specific retail supply chains are poorly positioned to respond if or when one arrives. As the research shows, only 32% of retail respondents are fully prepared to implement changes immediately if conditions deteriorate, the lowest rate of any sector in the research.

CUSMA/USMCA coverage is also constrained for retail because most sourcing originates in APAC, meaning even companies that want to expand certification have limited eligible product to work with. The protections that industrial and healthcare companies have built through rigorous certification programs are largely out of reach for retail companies whose supply chains were built around Asian manufacturing.

The differing pressures on each country adds another layer of complexity. Canadian retail respondents are more aware of the stakes than their U.S. peers but less resourced to act on that awareness. U.S. retail companies are more likely to feel prepared and they’re less directly exposed to a negative outcome since they have stronger domestic market alternatives. The preparedness gap runs across both borders, but it cuts deepest in Canada.

Read the full global trade report

How retail companies plan to insulate themselves from future tariff impacts

Retail shows more hesitation than other sectors when it comes to making significant structural changes to their operations and supply chains. Uncertainty has made capital commitments feel risky when the rules governing cross-border e-commerce could shift again without warning. Many Canadian companies are weighing fulfillment and warehouse investments in the U.S. to combat the elimination of de minimis, but they’re holding back until they know whether a distribution presence that makes sense today will still make sense after July’s review.

But this doesn’t mean retail companies are being passive in their response to tariffs. They’re planning more of the same operational changes that are already underway: adjusting routing, changing suppliers to lower-tariff countries and investing in strategic customs practices.

Between countries, the largest difference is in strategic customs investment: U.S. retail companies plan to invest at nearly double the rate of their Canadian peers (45% vs. 24%). U.S. companies are also more likely to report no expected pricing changes in the 18 months (16% vs. 7% for Canadian companies). For U.S. retailers, it appears that compliance infrastructure is being treated as a cost management tool that doesn’t require them to dismantle and rebuild retail supply chains. Meanwhile, Canadian retailers that face more immediate operational pressure seem to be focusing on routing changes and market exits rather than long-term compliance investments.

What retail shippers need from their logistics partners

Retail companies are more dependent on their broker and cross-border shipping partners for trade intelligence than any other sector in this research. That dependency is partly structural because retail has less internal compliance infrastructure than industrial or technology companies, and partly a result of the de minimis disruption, which landed fast and required guidance that many retailers didn’t have in-house.

Seventy-eight percent of retail companies say they feel supported by their shipping partners, with no major regional differences, although Canadian companies more often report feeling neutral rather than actively supported. As for what retail shippers specifically want from cross-border shipping partners, the research is clear:

- 58% want details on the potential impact of CUSMA/USMCA certification on their business

- 53% want proactive support on reducing tariff fees by analyzing their shipments

- 51% want consulting on operational adjustments they can make to reduce tariff impacts

- 50% want support obtaining CUSMA/USMCA certification (especially Canadian companies: 59% vs. 41% in the U.S.)

Retail companies aren’t looking for high-level trade guidance. They want a partner that understands their industry’s specific exposure—including the end of de minimis exemptions, APAC sourcing restrictions, low certification rates relative to other sectors and more—and shows up with solutions catered to that reality rather than generic advice that applies equally to every shipper.

The qualitative feedback from North American retail shippers is direct about where carriers could provide better support. Many companies across industries—retail included—depend on their cross-border shipping partners as their primary source of trade intelligence, but during peak tariff volatility, many found those partners slow to communicate and inconsistent in their guidance. For a sector that’s dependent on external expertise, that poses a risk to business continuity.

How Purolator can help retail companies get ready for July’s CUSMA/USMCA review

Retail is the sector where the awareness gap is widest, where the end of de minimis has already changed the economics of cross-border e-commerce and where only 32% of companies are ready to act immediately if conditions shift further. Entering the CUSMA/USMCA review unprepared is higher stakes for retail than for any other industry in this research.

For retail companies that are ready to get ahead, start by mapping your current CUSMA/USMCA eligibility by SKU to understand where certification could reduce your duty exposure. Then build options for U.S.-based distribution and make sure your shipping partner is proactively finding solutions for your specific challenges.

How Purolator supports retail shippers

Purolator built its retail and e-commerce solutions around the exact challenges North American shippers are facing today.

For de minimis disruptions

Purolator has a dedicated response for the change that hit retail harder than any other sector. A consolidated customs brokerage option reduces per-shipment fees for high-volume, lower-value shipments, addressing the cost structure that made cross-border e-commerce viable under the old exemption. Purolator’s acquisition of Livingston International, a dedicated e-commerce customs practice with automated pre-clearance workflows and bulk classification tools, provides the throughput and compliance accuracy that high-volume retail shippers need under formal entry requirements.

For CUSMA/USMCA certification

The Purolator Trade Assistant helps retail shippers identify HS codes and determine which products qualify for CUSMA/USMCA protection. For retailers whose certification coverage is constrained by APAC sourcing, this tool helps find eligibility within an existing product mix rather than restructuring it. Livingston International’s brokerage expertise supports the documentation and validation work that converts eligibility into actual duty savings.

For network and fulfillment

Purolator delivers to 100% of Canadian postal codes and offers warehousing and fulfillment services for Canadian retailers evaluating whether a U.S. distribution presence makes sense in a post-de minimis environment. This is one of the most important decisions Canadian retail companies are forced to make. Having a partner that supports both sides of the equation can simplify the evaluation.

For returns

Purolator offers reverse logistics including sort, repackage and refurbish services, trackable cross-border returns and package-free and label-free returns at select retail access points. This is a meaningful differentiator in a sector where returns volumes are high and the customer returns experience directly affects brand loyalty.

For cross-border complexity and Mexico routing

For Canadian retailers exploring Mexico as a CUSMA/USMCA-compliant alternative to direct Canada-U.S. border exposure, Purolator’s integrated North American network covers the full continent—Canada, the U.S. and Mexico—with LTL and TL freight options, end-to-end customs support and bilingual trade compliance specialists who understand CUSMA documentation requirements at every border. With access to 2,700+ trade experts and 55+ border entry points across North America, the expertise to navigate a more complex routing environment is already in place.

Want to learn what the CUSMA/USMCA review means for global supply chains? Download the full report

Retail is carrying a sector-specific burden that other industries aren’t feeling in the same way, absorbing general tariff pressure while rebuilding cross-border e-commerce operations around a post-de minimis reality. Only 32% of retailers are fully prepared to act immediately if conditions get worse. And the CUSMA/USMCA review adds another layer of uncertainty for a sector that already has the lowest awareness of what’s coming.

The retail companies best positioned for what’s to come are the ones that have mapped their CUSMA/USMCA eligibility, built distribution options on both sides of the border and deepened their relationship with a proactive e-commerce logistics partner. For the cross-border shipping complexity that’s sure to surface after the review, Purolator is here with retail and e-commerce expertise so retailers don’t have to act alone.

*This research was commissioned (paid for) by Purolator and conducted by HelloInfo, an independent research firm. Purolator was not identified as the sponsor during data collection.